REAL ESTATE TAX TIPS

INTERNAL REVENUE CODE SECTION 1031 AND DEALING WITH LIKE-KIND EXCHANGES

According to the IRS:

In general, if you exchange business or investment property solely for business or investment property of a like-kind, no gain or loss is recognized under Internal Revenue Code Section 1031.

BUT

If, as part of the exchange, you also receive other (not like-kind) property or money, gain is recognized to the extent of the other property and money received, but a loss is not recognized.

Keep In Mind: Section 1031 does not apply to exchanges of inventory, stocks, bonds, notes, other securities or evidence of indebtedness, or certain other assets.

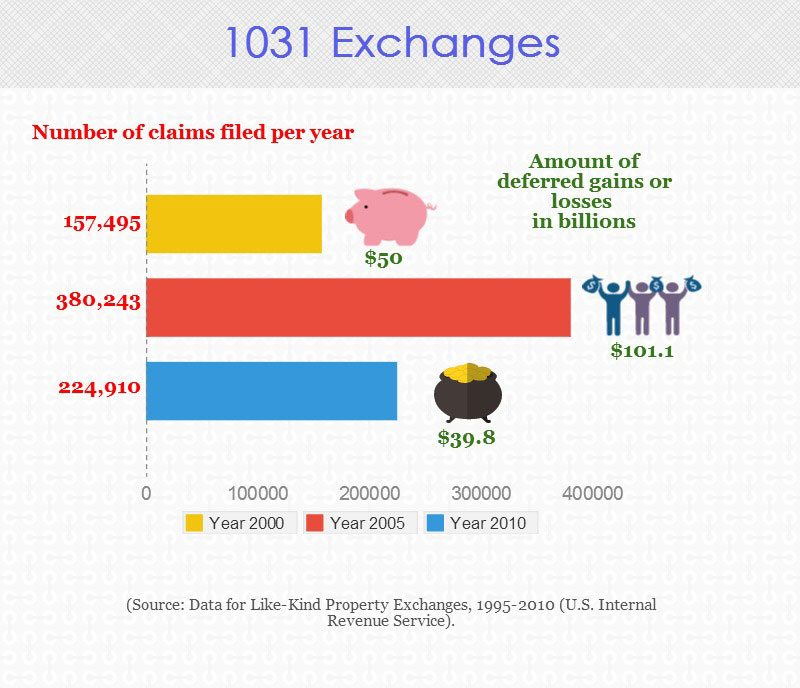

In 1979, this section was expanded to include non-simultaneous sale and purchase of real estate. Therefore, the purchases do not have to be at the same time to qualify.

HOW DO I KNOW IF MY PROPERTIES ARE CONSIDERED “LIKE-KIND”?

Your properties are of Like-Kind if they are:

- Of the same nature or character (even if they differ in grade or quality)

- Personal properties of the same class

- Real properties, regardless of whether they are improved or unimproved

Your properties are not of Like-Kind if they are:

- Livestock of different sexes

- Personal property used predominantly in the US & personal property used outside the US

- Real property inside and real property outside the US

OTHER IMPORTANT FACTS

- Taxpayers who hold real estate as inventory, or purchase for re-sale are considered “dealers”. These properties are not eligible for Section 1031 treatment.

- However, if a taxpayer is a dealer and also an investor, she/he can utilize Section 1031 on qualifying properties. Personal use property will not qualify for Section 1031.

- Cash to equalize a transaction cannot be deferred under Code Section 1031 because it is not of like kind. This cash is commonly referred to as the “boot” in real estate transactions and is taxed at a normal capital gains rate.

- The property to be exchanged must be identified within 45 days, and received within 180 days

WHAT IS BOOT?

- It is not used in the Internal Revenue Code, the term “Boot” is commonly used in discussing the tax implications of a 1031 Exchange.

- Boot is an old English term meaning “Something given in addition to.”

- “Boot received” is the money or fair market value of “Other Property” received by the taxpayer in an exchange. Money includes all cash equivalents, debts, liabilities or mortgages of the taxpayer assumed by the other party, or liabilities to which the property exchanged by the taxpayer is subject.

- “Other Property” is property that is non-like-kind, such as personal property, a promissory note from the buyer, a promise to perform work on the property, a business, etc

DOES MY SECOND HOME FALL UNDER SECTION 1031?

Many are left confused if the purchase of a second home is impacted by section 1031.

The answer?

“The Service has ruled that properties that are purchased for personal use are NOT investment properties, and therefore do not qualify for Section 1031 treatment.”

If you live in the home at anytime, it will be not be classified as an investment property.

TIME LIMITATIONS

The 1031 exchange begins on the earliest of the following:

- the date the deed records, or

- the date possession is transferred to the buyer,

and ends on the earlier of the following:

- 180 days after it begins, or

- the date the Exchanger’s tax return is due, including extensions, for the taxable year in which the relinquished property is transferred.

The identification period is the first 45 days of the exchange period. The exchange period is a maximum of 180 days. If the Exchanger has multiple relinquished properties, the deadlines begin on the transfer date of the first property. These deadlines may not be extended for any reason, except for the declaration of a Presidentially declared disaster.

AN ALTERNATIVE WORTH CONSIDERING

We thought you’d like to know:

“A “Structured Sale Annuity” or “Ensured Installment Sale” is a capital gains tax deferral tool that enables the seller to gain benefits that other sales and capital gains deferral methods do not offer. It is a hybrid of the common installment sale and a structured annuity, and it enables the seller to collect a stream of payments, leverage equity, earn a pre-tax return, and other benefits. This method is a tool for those who want to do a 1031 exchange but cannot find a property within the time frame, and it allows the seller to have a backup plan. However, the capital gains taxes due on the property will still be due once each installment payment is made, thus causing the taxpayer to still pay the tax.”

Sources: https://en.wikipedia.org/wiki/Internal_Revenue_Code_section_1031